To obtain the best experience, we recommend you use a more up to date browser .

China’s CO2 emissions reductions have been substantial: by 2020, carbon intensity decreased by 48.4% compared to 2005 levels, achieving objectives outlined in the Nationally Appropriate Mitigation Actions and Nationally Determined Contributions.

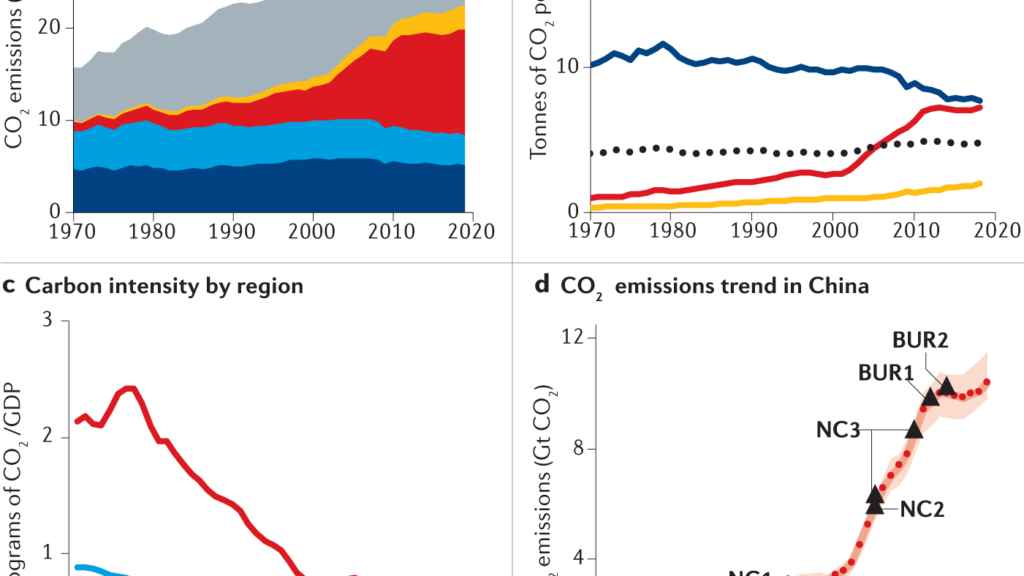

Owing to its rapid economic development and urbanization, China is currently the largest carbon emitter in the world, accounting for 28% of global CO2 emissions in 2019 .

China’s share in global CO2 emissions has increased rapidly since about 1980, with emissions per capita increasing substantially during the 2000s, but plateauing and fluctuating since 2010.

Building on these objectives, in September 2020, President Xi further proposed a long-term mitigation goal of carbon neutrality before 2060, and in December 2020, enhanced the INDC targets to a >65% reduction in carbon intensity by 2030 from 2005 levels.

These include increasing the share of non-fossil energy, developing negative emission technologies, and measures to remove carbon from the air or to increase the carbon sink.

We subsequently assess China’s achievements towards low-carbon development, and discuss future prospects and challenges for further decarbonization, including reaching peak emissions before 2030 and achieving carbon neutralization before 2060.

Before 1970, China’s total CO2 emissions were <900 Mt CO2, and per capita emissions were roughly a quarter of the global average9.

Rapid industrialization has also established China as the world’s manufacturing powerhouse.

For example, provinces that are located within industrial clusters, such as Shandong and Hebei, exhibit a higher proportion of CO2 emissions from manufacturing sectors, especially from the production and smelting of non-metals and metals25.

For instance, the carbon intensities of Shanxi, Inner Mongolia and Ningxia are roughly 6, 7 and 14 times greater than that of Beijing in 2018, respectively12.

Owing to the fast growth of emissions and large amount of coal consumption, this uncertainty dominates the overall uncertainty from developing countries11,29,195,196.

However, keeping emission factors up to date is a key challenge to obtain reliable emission estimates200, particularly as China increases its overall coal consumption each year by using coal of a different quality mix.

The increase in China’s CO2 emissions can be ascribed to its rapid economic growth and improving living standards31,32. Between 1978 and 2018, emissions resulting from the growth of GDP per capita were 176% higher than the overall change in CO2 emissions, completely offsetting the effects of improved energy intensity 32.

After joining the WTO in 2001, export was a temporary key contributor to emissions growth in China, accounting for nearly half of the annual emissions growth from 2002 to 2005 .

This upgrade in South–South trade and the reallocation of low-end manufacturers from China to other developing countries could introduce additional global emissions owing to the higher emissions intensity in developing countries45,46,47.

Moreover, trade conflict could result in the isolation of western nations with regard to the global high-tech industrial chain, which could increase the difficulty of transitioning China to a low-carbon economy.

Although trade dominated emissions in the early 2000s, thereafter investment became the primary factor .

As a result, annual crude steel production, cement production and energy consumption increased by 14%, 15% and 5%, respectively, in 2009, contrasting with 3%, 5% and 3% in 2008 .

This regulatory change triggered a surge in thermal power plant construction, reportedly adding more than 250 GW of new power capacity between 2014 and 2018; 78% of these projects were coal power plants.

In response to the COVID-19 pandemic, the Chinese government further proposed a set of stimulus projects to boost economic growth54, investing over 30 trillion yuan .

Living standards in China have improved dramatically since the 1970s: as of 2017, per capita disposable income was 22.8 times higher compared to 1978 .

For instance, cities in eastern coastal provinces have relatively higher household carbon footprints61: the top 5% of the population with the highest income in China contribute nearly 20% of the total household carbon footprint.

CO2 emissions induced by government consumption contributed 7%, 5%, 5% and 6% to the national CO2 emissions in 2002, 2007, 2012 and 2017 respectively35.

China has now entered a “new normal” phase in terms of its economic development, transitioning from an investment-driven economy to a consumption-driven economy35,62.

Owing to the magnitude and rapid growth of China’s CO2 emissions — attributed to factors such as trade, consumption and investment — several policy-based mitigation approaches have been introduced to facilitate their reduction.

A major contribution towards curbing carbon emissions in China has involved voluntary climate change commitments.

The Chinese government has thus embarked on several key tasks, including building a clean energy system, implementing energy conservation and emission reduction actions in different sectors, accelerating carbon emission trading and green financing, improving the capacity of ecological carbon sinks, advocating a low-carbon lifestyle among the public, strengthening international cooperation, and building a green “silk road”.

Accordingly, provinces might formulate specific implementation plans, as well as their own targets of reducing energy intensity and increasing the share of non-fossil energy consumption.

At the provincial level, most provinces successfully decreased their carbon intensity year by year, as specified by the 13th FYP, in some cases achieving and even exceeding the targets .

Data of carbon intensity trend are collected from the IPE12, which are originally from the China City Greenhouse Gas Working Group; data for Tibet is not available.

However, some provinces were not able to achieve their goals, such as Inner Mongolia, where carbon intensity decreased by 14% in 2020 compared to 2015 levels, thus missing the target of −17% .

Increasing capacity, improving energy efficiency per unit production in the production process, and deploying and transforming low-carbon technologies all helped reduce carbon intensity per unit of economic output.

Replacing such power plants with those that are larger and more efficient did substantially increase the total energy efficiency, but the scale-up in fossil fuel-based power generation has resulted in only a marginal reduction in energy intensity.

Contributions of each component are collected from the IEA World Energy Outlook’s Sustainable Development Scenario66,67, where ‘Efficiency’ denotes end-use efficiency and fossil fuel subsidies reform, and ‘Negative emission needed’ covers nuclear, CCUS and other technologies66.

Moreover, the construction of 210 new coal projects in 2015 following the decentralization of power plant approval77, the fact that most existing coal-fired power plants have been put into operation in the past 15 years78 and the approval of coal projects to boost economic growth following the COVID-19 pandemic all provide additional challenges to be met before China’s coal consumption and emissions can peak.

These changes are consistent with government commitments to control coal-fired power generation projects and to limit the increase in coal consumption during the 14th and 15th FYPs.

During the 13th FYP, non-fossil energy installed capacity grew at an average annual rate of 13.1%79, allowing the targets of 15% non-fossil energy to be met .

Such a large-scale expansion of renewable energy necessitates fundamental changes in energy infrastructure, such as storage and transmissions, and calls for the energy market to integrate high penetration of renewables with grids.

This large range creates a huge gap that otherwise will need to be filled by solar, wind or CCUS in a low nuclear scenario85,89,90.

As such, adoption of technology, changes in human behaviour and policy measures that increase energy efficiency and restrain demand are equally important at the other side of the transition to clean energy.

Indeed, efforts to expand afforestation have made it the largest contributor , accounting for nearly 45% of anthropogenic emissions102.

Under these circumstances, advanced water resource management and treatment technologies, along with precision agriculture and land-use management, could be deployed to ensure that most, or all, of the increased biomass in the afforested areas is preserved indefinitely103.

Carbon sinks in open seas are much larger, with preliminary estimates suggesting that sedimentary organic carbon storage in marginal seas of China’s coastal shelf is 75.1 Mt CO2 per year and that primary productivity of large-scale culture algae in China is approximately 12.9 Mt CO2 per year107.

For example, the potential capacity for CO2 storage in China is estimated to be 1,800 to 3,000 Gt CO2 , with an annual maximum capture capacity of around 0.82 Mt CO2, accounting for approximately 2% of global CCS storage113.

Thus, to have a more important role in China’s carbon neutrality, CCUS technologies must be developed rapidly and both CCS and bioenergy combustion with CCS facilities need to be deployed on a large scale as soon as possible.

It is of top priority for both central government and local governments to devise and enforce the corresponding regulations and laws.

Direct air capture technology is emphasized as one of the most important negative-emission technologies, with large-scale potential of CO2 removal; these physically or chemically adsorb CO2 in the air directly122,123.

Some cities might rely heavily on imported energy and products to meet their consumption, but this means that their emissions have just been transferred to other cities.

Region-specific CO2 emission reduction targets could be set in provinces and cities145.

Given the scale of China’s “green market” and the timing of its transition to a higher-value-added economic structure, market reforms associated with environmental protection could bring tremendous change.

The plan initially started in the power industry, and was planned to expand to seven major industries, making it the largest emission trading scheme worldwide162. In 2020, China’s Ministry of Ecology and Environment drafted rules for the national carbon emission trading scheme, further leading an expansion of emission trading schemes from these pilots to other regions nationwide.

Indeed, with large-scale deployment of renewable power generation, particularly hydro, wind, and solar, the share of fossil fuel has reached an all-time low and coal consumption has plateaued.

In doing so, several national targets have been met: as of 2020, carbon intensity was reduced by 18.8% relative to the 2015 level, the share of non-fossil consumption as part of the total primary energy consumption was increased to 15.9%, and forest stock volume was increased to over 17.5 billion m3, exceeding the targets of 18%, 15% and 16.5 billion m3, respectively.

Milestones in achieving the national 2060 carbon neutrality target include the following: establishing a full-scale cap-and-trade system that covers all sectors, achieving negative emissions from afforestation, recycling and CCUS; recycling 100% of construction materials and industrial byproducts; realizing the goal of a 70% or 85% non-fossil share of primary energy consumption by 2050 under the 1.5° C and 2° C temperature limit scenarios, respectively; and developing a full CCUS for the remaining fossil fuel-based boilers and plants.

Before achieving any breakthroughs in applying renewable energy technology at large scale, as well as the technology of utilizing coal in a clean way, China still needs to find a balance between coal phase-out, costs and energy security.

Incorporating carbon neutrality into national social and economic plans will accelerate optimization and green upgrading of industrial structure and energy structures, and promote the development of new technologies for low-carbon industries.

Digital technologies are also expected to revolutionize both the demand and the supply side of energy systems. Great challenges lie ahead in terms of social cost and political stability in the course of this dramatic transition of the energy and economic systems, which will create both winners and losers at large scale.

Source data supported high resolution carbon emissions inventory for urban areas of the Beijing–Tianjin–Hebei region: spatial patterns, decomposition and policy implications.

Potential co-benefits of electrification for air quality, health, and CO2 mitigation in 2030 China.

Scenarios of energy efficiency and CO2 emissions reduction potential in the buildings sector in China to year 2050.

Mode, technology, energy consumption, and resulting CO2 emissions in China’s transport sector up to 2050.

The stage-classified matrix models project a significant increase in biomass carbon stocks in China’s forests between 2005 and 2050.

Carbon sequestration potential of forest vegetation in China from 2003 to 2050: predicting forest vegetation growth based on climate and the environment.

Development of a tree growth difference equation and its application in forecasting the biomass carbon stocks of chinese forests in 2050.

Assessment of CO2 storage potential and carbon capture, utilization and storage prospect in China.

Analysis of drivers and policy implications of carbon dioxide emissions of industrial energy consumption in an underdeveloped city: the case of Nanchang, China.

A top-bottom method for city-scale energy-related CO2 emissions estimation: a case study of 41 Chinese cities.

Standardization of the evaluation index system for low-carbon cities in China: a case study of Xiamen.

Co-benefits of China’s climate policy for air quality and human health in China and transboundary regions in 2030.